Having a credit score of 686 puts you in the “good” credit range, which means you have access to most loans, but may not always get the very best rates or terms. Here’s an overview of the most common types of loans and what you can expect to qualify for with a 686 credit score.

Overview of 686 Credit Score

-

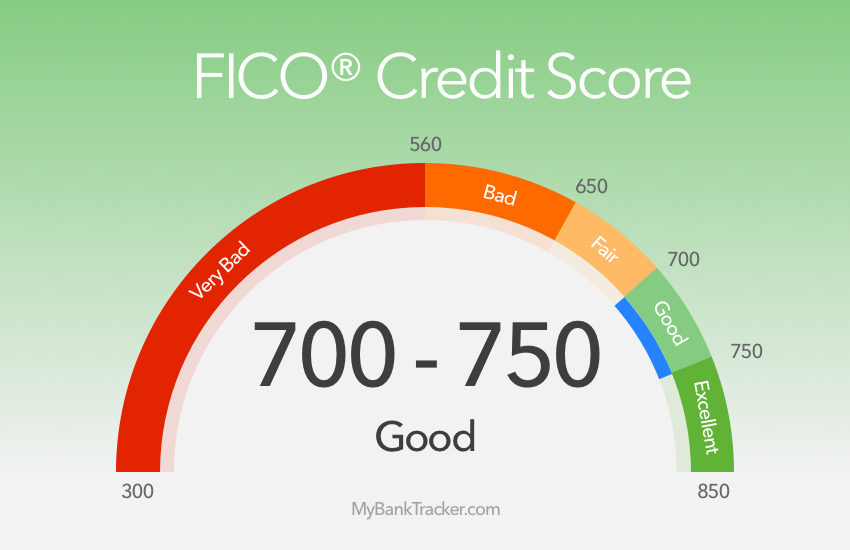

FICO says that a credit score of 686 is “good.” It is just below the range of 670-739 that they call “very good.”

-

You can get most loans with a credit score of 686, but you won’t always get the best terms or lowest interest rates that people with higher scores get.

-

Lenders think that borrowers with scores of 686 are pretty low-risk, but they may see that these people could do a better job of managing their debt and making payments on time.

-

If you raise your score above 700, you’ll be able to get better loan rates and options. Pay down your balances, don’t be late on payments, and check your credit report for mistakes.

Personal Loans

-

Most online lenders will approve personal loans for borrowers with credit scores around 686. Approved amounts often range from $1,000 to $40,000.

-

Interest rates on personal loans for 686 credit scores generally fall between 10% and 20%. The higher your score, the lower rate you can qualify for.

-

Lenders like LendingClub, Prosper, Lightstream, and Upgrade offer personal loans to borrowers with good credit. Pre-qualification tools can give you an idea of your rate.

-

Take time to compare offers from multiple lenders. Look for the lowest APR and best terms for your situation before applying.

-

Avoid payday loans or high-interest personal loans. These can lead to much higher rates and make it harder to improve your credit.

Mortgage Loans

-

Conventional mortgage lenders generally require a minimum score of 620, so a 686 credit score meets this threshold.

-

However, a 686 score will not get you the best mortgage rates. Interest rates are still likely to be near the upper limit for a conventional loan.

-

Expect to pay 0.5 to 1 percentage point higher on your mortgage rate compared to someone with a score of 740 or above, all else being equal.

-

Improving your score before applying for a mortgage can help you land better rates, lower fees, and more favorable loan terms.

-

Shop around with different lenders to see what programs may be available for your situation. Compare offers carefully.

Auto Loans

-

Auto loans are readily available with a 686 credit score from most major lenders such as credit unions, banks, and the automaker’s financing division.

-

You can expect average interest rates between 4% and 7% for a used car loan with good credit. New car loans tend to have lower rates.

-

Your actual rate will depend on other factors too like your debt-to-income ratio, loan term, loan amount, and the vehicle.

-

Having a steady income, reasonable debt levels, and substantial down payment will improve your chances of getting approved and securing better terms.

-

Pre-qualifying with lenders can help you determine if you will get approved and compare loan terms. Expanding your options leads to better rates.

Student Loans

-

Federal student loans do not require a credit check, so your 686 score is not a factor. All applicants can qualify for federal loans like Direct Subsidized, Unsubsidized, and PLUS loans up to the annual/aggregate limits.

-

Private student loans are credit-based. Lenders like Sallie Mae, College Ave, and Citizens Bank offer private loans to borrowers with good credit scores.

-

Interest rates on private student loans for borrowers with 686 credit score range from about 4% to 8% fixed. The higher your score, the lower your rate.

-

You typically need a cosigner for private student loans if you have limited credit history. This places the responsibility for repaying the loan on the cosigner too.

-

Make sure to compare rates and terms from different private lenders before applying for a private student loan.

How to Improve from a 686 Credit Score

While a 686 credit score provides access to most loans, boosting your score further will lead to better loan terms over your lifetime. Here are some tips:

-

Review credit reports and dispute any inaccuracies that may be hurting your score. Errors can drag down your credit.

-

Pay down revolving balances like credit cards to lower your credit utilization ratio. Below 30% is good.

-

Become an authorized user on someone else’s credit account to inherit their solid payment history.

-

Open a new credit card and use it responsibly by paying on time and keeping balances low. This demonstrates good credit management.

-

Enroll in automatic payment plans on loans and credit cards to avoid ever missing payments in the future. One skipped payment can be very damaging.

-

Limit new credit applications. Too many hard inquiries from applying for financing can ding your score temporarily.

With a disciplined approach and some time, you can steadily work on improving your 686 credit score. Aim for breaking above 700, which will unlock better loan opportunities. Monitor your credit with free services and check progress periodically. Maintaining good credit habits makes a long-term difference.

Upstart : Best for borrowers with limited credit history

- View detailsHide details

Qualifications:

Key Facts:Upstart personal loans offer fast funding and may be an option for borrowers with low credit scores or thin credit histories.Qualifications:

- Must be a U.S. citizen or permanent resident living in the U.S.

- Must be at least 18 years old in most states.

- Must have a valid email address and Social Security number.

- Must have a full- or part-time job, a full-time job offer starting within six months or another source of regular income.

- Must have a personal bank account at a U.S. financial institution with a routing number.

- No bankruptcies in the last 12 months.

- No current delinquent accounts on your credit reports.

- Fewer than six hard inquiries on your credit report in the last six months, excluding student, auto and mortgage loans.

- Minimum credit score: None.

- Minimum annual income: $12,000.

Available Term Lengths:3 to 5 yearsFees:

- Origination: 0% to 12%.

- Late fee: 5% of the unpaid amount or $15, whichever is greater.

- Insufficient funds fee: $15.

Prosper : Best for easy application process

- View detailsHide details

Qualifications:

Key Facts:Prosper offers rates and fees that compare to other lenders for fair- and good-credit borrowers.Qualifications:

- Minimum credit score: 660; borrower average is 709.

- Minimum income: $15,000; borrower average is $137,000.

- Maximum debt-to-income ratio: 50% (excluding mortgage); borrower average is 41.05% (including mortgage).

- Must be at least 18 years old.

- Must provide Social Security number and a U.S. bank account.

Available Term Lengths:2 to 5 yearsFees:

- Origination fee: 1% to 9.99%.

- Late fee: The greater of $15 or 5% of the unpaid amount.

- Insufficient funds fee: $15.

- Mailed-in payment fee: $5.

Is A Credit Score Of 686 Good? – CreditGuide360.com

FAQ

How much of a loan can I get with a 686 credit score?

For FICO, a fair or good credit score is between 580 and 739. For VantageScore, a fair or good credit score is between 601 and 780. Many personal loan lenders offer amounts starting around $3,000 to $5,000, but with Upgrade, you can apply for as little as $1,000 (and as much as $50,000).

What can I do with a 686 credit score?

Lending Options with a 686 Credit ScoreCredit Cards. You may qualify for a variety of unsecured credit cards, including some with decent rewards. Auto Loans. Personal Loans. Mortgages. Pay Your Bills On Time. Lower Your Credit Utilization Rate. Avoid Applying for Too Much Credit at Once. Keep Old Accounts Open.

What credit score do I need for a $10,000 personal loan?

Requirements will vary across lenders. However, qualifying for a $10,000 personal loan typically requires a credit score that exceeds 640, an active checking account, and a steady, verifiable income, among other factors.

What credit score do I need to get a $40,000 loan?

The best chances of getting a $40,000 loan are if you have at least a 740 credit score and a DTI ratio of 336 or less. May 21, 2025.