More and more people are using tradelines as a quick way to raise their credit scores. But should you really buy tradelines? In this detailed guide, we’ll look at the pros, cons, legalities, and other options to give you a full picture.

What are Tradelines?

Any account that shows up on your credit report is called a tradeline. This includes credit cards, loans, mortgages, and more. The creditor’s name, account status, credit limit, balance, and payment history are all shown on each tradeline.

Tradelines are a key factor in calculating your credit score. More tradelines with positive payment histories and low balances can raise your score. Too few or negative tradelines can lower it.

With tradeline purchasing, you pay to be added as an authorized user on someone else’s credit card. This gives you the benefit of their positive payment history without being financially responsible for the account.

The Potential Benefits of Buying Tradelines

Quick credit score boost – Being added to an old account with a solid history can provide a big boost, especially if your own file is thin Scores can potentially increase by 50-100 points.

Establishes credit history – For those with limited credit history, purchased tradelines create an instant positive track record. This makes you appear less risky.

Increases total credit limits – Getting added to accounts with high limits, even if you can’t use them, reduces your overall credit utilization ratio. This factor accounts for 30% of credit scores.

Adds account mix—Tradelines let you spread out your credit between accounts that are revolving (like credit cards) and accounts that are fixed (like loans). This 10% factor improves credit diversity.

Fast process – It can take months or years to build credit naturally. Tradelines provide a short-cut for an immediate boost within weeks.

The Potential Downsides of Purchased Tradelines

Pricey—Prices change based on credit history and limit, but expect to pay $500 to $1500 per tradeline. Adding multiple can get costly.

Temporary – The effects fade when you’re removed as an authorized user after a few months. The account itself may stay on your report up to 10 years.

No substitute for credit skills – While scores may increase, you don’t learn responsible habits like making payments or limiting balances.

Legality concerns – While not explicitly illegal, the CFPB and FTC frown upon the practice as misrepresenting your creditworthiness.

Lender distrust – Many lenders view purchased tradelines as “gaming the system” and may deny applications because of them.

Scam risk – Sharing personal info like your SSN to buy tradelines poses identity theft dangers if dealing with unreputable sellers.

Credit freezing – Accounts you buy may become frozen if investigations detect suspicious authorized user activity. This could negatively impact the seller.

Score variability – Not all scoring models weigh authorized user accounts equally. For example, the FICO 8 model excludes them.

The Legality of Buying Tradelines

There are no laws explicitly prohibiting the purchase of tradelines. However, the Fair Credit Reporting Act does prohibit false or misleading information appearing on credit reports. Both the Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC) have expressed concerns that purchased tradelines essentially “misrepresent” your true creditworthiness.

While rare, some cases of bank fraud charges have emerged when applicants fail to disclose purchased tradelines on credit applications. However, as long as you fully disclose any purchased tradelines if asked by lenders, you should avoid legal risks. But be aware that lenders may view your application unfavorably if they know you bought tradelines.

The CFPB has also warned that the practice may violate Equal Credit Opportunity laws by promoting discrimination. For example, low-income applicants may not be able to afford purchasing tradelines available to wealthier applicants.

Alternatives to Buying Tradelines

While purchased tradelines promise quick credit score fixes, responsible credit habits provide longer-lasting benefits:

Become an authorized user – Ask a family member or friend with a long positive history to add you to their account. Avoid paying them.

Open a secured card – These require a refundable deposit and help establish payment history.

Use credit builder loans – Make payments towards savings while simultaneously building credit history.

Pay down balances – Lowering credit utilization immediately improves credit scores as balances drop.

Dispute errors – Fixing mistakes on your reports provides a score boost. Monitor your reports regularly.

Practice good habits – Make on-time payments, keep balances low, and avoid unnecessary debt. Healthy habits over time are most effective.

The Bottom Line: Approach Tradelines Carefully

While purchased tradelines can provide a meaningful credit score lift in some cases, they come with substantial risks and drawbacks that make them questionable at best for many consumers. Improving through responsible habits takes longer but offers true skill-building and long-term benefits.

If you do choose to buy tradelines, exercise extreme caution in researching sellers, protecting personal information, and scrutinizing “too good to be true” deals. And avoid viewing purchased tradelines as a substitute for developing lasting positive behaviors.

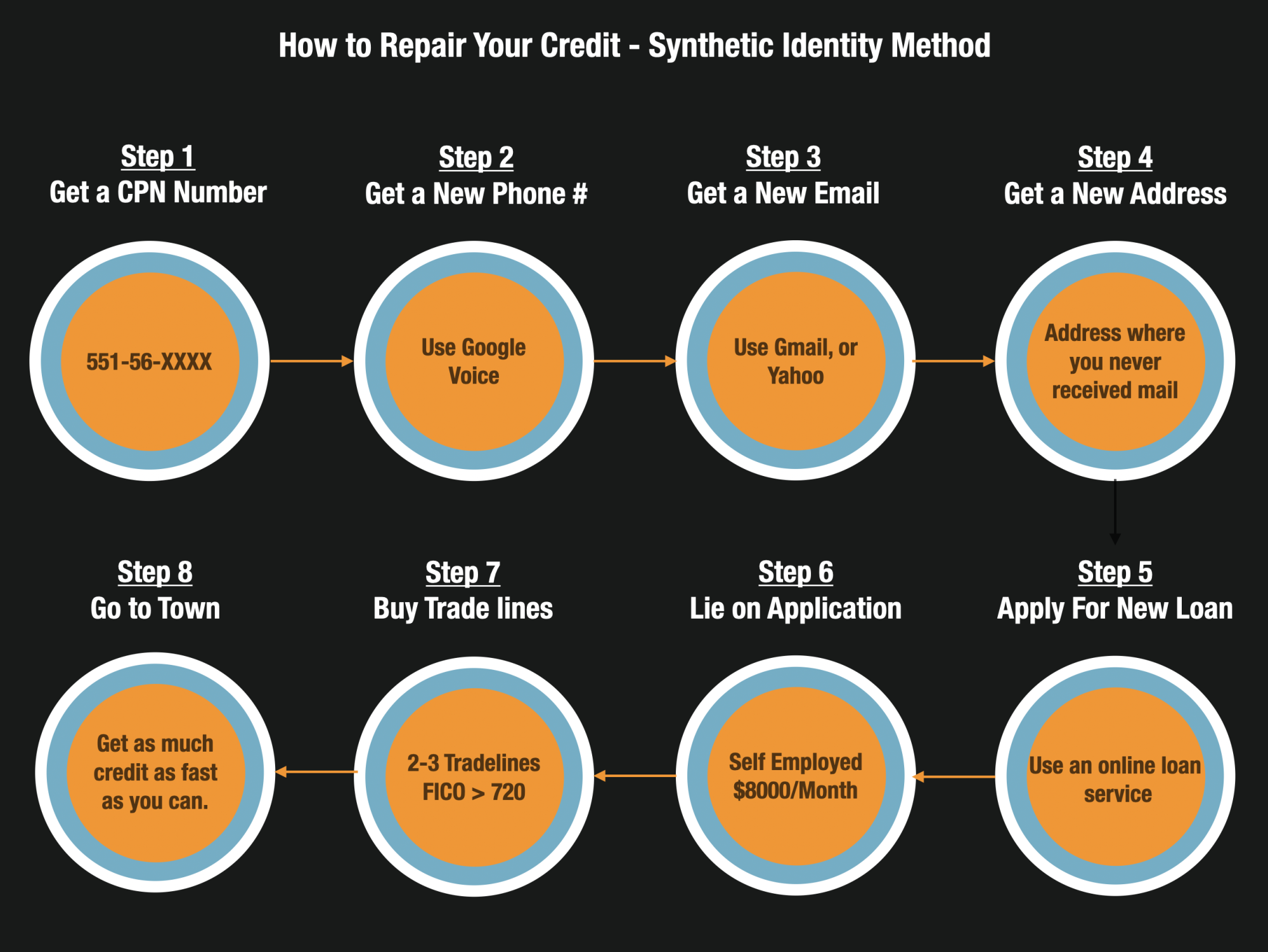

How Buying Tradelines Works

A tradeline is another name for a credit account that shows up on your credit reports. Each loan and credit card has a separate tradeline that includes various information about the creditor and the account.

Buying a tradeline involves paying someone to add you to one of their credit accounts, typically as an authorized user on a credit card. Because many credit card companies report account activity to the credit reporting agencies (Experian, TransUnion and Equifax) for both the primary cardholder and authorized users, their positive account history can potentially help improve your credit.

Tradeline companies act as intermediaries, connecting buyers and sellers for an additional fee. Depending on the accounts credit limit and age, the cost can range from a few hundred dollars to upwards of $1,000.

Youll also need to provide a copy of your drivers license and your Social Security number. Once youve completed the process, youll be added to the sellers tradeline for a couple of months, after which youll be removed. The account will remain on your credit report as “closed” and can remain on your report for up to seven years.

Dispute Credit Report Inaccuracies

If there are erroneous or fraudulent tradelines on your credit reports, they could bring down your credit score. Get a free copy of your report from each of the credit reporting agencies through AnnualCreditReport.com and review them for potential problem accounts.

You can also monitor your FICO® ScoreΠand Experian credit report more regularly through Experians free credit monitoring service.

If you find errors on your report, you have the right to dispute them directly with the credit reporting agency, as well as with the creditor. If the credit bureaus confirm your dispute and either remove or correct the information, your credit score will respond accordingly.

Credit TRADELINES: Pros and Cons

FAQ

Why should I learn about tradelines?

Learning about tradelines can help you do a more thorough review of your credit reports. What Is a Tradeline? Be aware that negative information may remain on your tradelines for seven to 10 years. A tradeline is an account that’s listed on your credit report. Your credit score is calculated using the tradelines in your credit report.

What is a tradeline & how does it work?

Tradelines mostly do two things: they show lenders how you’ve used different types of credit in the past and give credit bureaus information they need to make your credit score. List of Account Types for Each Tradeline: This could be a credit card, student loan, mortgage, or any other type of credit.

Should I buy a tradeline?

Buying a tradeline is sometimes presented as a credit repair strategy. It involves paying a third-party service to add you to another person’s tradeline, so that their tradeline information appears on your credit report, represented as your own. These are short-term agreements, so you’re removed from the tradeline after a designated amount of time.

Are tradelines bad for your credit?

Here are some risks to be aware of: Tradelines that you can’t pay on time or use too much of your credit can lead you to develop a poor payment history or high credit utilization, which can harm your credit score rather than help it.

What is a tradeline on a credit report?

A tradeline is an account that’s listed on your credit report. Your credit score is calculated using the tradelines in your credit report. Review your credit reports often to make sure that all the account information is accurate. On your credit report, you’ll see a list of your credit accounts, which are referred to as tradelines.

Should I buy a tradeline If I have a low credit score?

They’re critical to your score. When you have a low credit score, it may be worth considering buying tradelines. Various third-party services charge a fee to add you as an authorized user on a credit account. This will show up as a tradeline on your credit report when you become an authorized user on an open account.

Do tradelines really help your credit?

Tradelines work exceptionally and over 33% of americans use them. They credit unions account for them when calculating your credit score, and they’re very well known for their positive effects on credit (both temporary or long-term).

How much will a tradeline boost my credit?

What are the risks of tradelines?

Tradelines that you can’t pay on time or use too much of your credit can lead you to develop a poor payment history or high credit utilization, which can harm …Mar 17, 2025

How long does it take a tradeline to hit your credit?

Most tradelines post within 15 to 45 days, depending on the type of account and the credit reporting agencies involved. You can speed up the process by choosing tradeline providers known for prompt reporting and maintaining timely payments on all your accounts.