When you apply for a loan or credit card, your credit score is one of the first things lenders look at. They check Equifax, Experian, or TransUnion, but which score do they look at? And why do scores vary so much from one bureau to the next? Read on to find out.

The Three Credit Bureaus

In the United States. there are three major consumer credit bureaus that collect your credit history and provide credit reports and scores to lenders

- Equifax

- Experian

- TransUnion

Each bureau maintains its own database of consumer credit information reported to them by lenders and creditors. This means each of your credit reports may contain different information, depending on which creditors report to each bureau.

As a result, you don’t have just one credit score – you have a separate score calculated by each bureau based on the data in their credit report.

Why Scores Differ Between Bureaus

There are several reasons why your credit scores can vary significantly across Equifax, Experian and TransUnion:

-

Different credit scoring models – While all three use FICO scores, there are many versions with slight variations in algorithms.

-

Incomplete reporting – Not all lenders report to all three bureaus, leading to discrepancies.

-

Reporting lags – Creditors report at different times of the month, causing temporary mismatches.

-

Credit report errors – Mistakes or outdated info on one report can lower that score.

-

Fraud issues – Identity theft incidents may only impact one report initially.

As a result, it’s common to see credit score differences of 50 points or more between Equifax, Experian and TransUnion.

Is Equifax or Experian Score Higher?

There’s no definitive answer on whether Equifax or Experian credit scores are higher on average. Each bureau has a different database of information that can cause scores to vary.

There are, however, some patterns that could make one score higher than the others:

-

Your Equifax score may be higher if a bad mark only shows up on Experian or TransUnion.

-

If you have late payments that haven’t been reported to all bureaus yet, your score may be higher at those missing the late payments.

-

If you have a new credit account that hasn’t been reported to all bureaus yet, your score may be temporarily higher where it’s not appearing.

-

If you have an error or mistake on one report, your score will likely be higher on the other two until you dispute and resolve it.

How to Check All Three Credit Scores

To understand why your scores differ and which one is most accurate, it’s important to check your credit reports and scores from all three bureaus. Here are some options to get all three:

-

AnnualCreditReport. com: Equifax, Experian, and TransUnion all offer free credit reports once a year. However, your scores will not be shown. Instead, it will show your full history at each bureau.

-

Credit monitoring services – Paid services like myFICO provide monthly access to your scores and reports from all three bureaus for comparison.

-

Credit cards – Many issuers like Discover now provide free FICO scores from all three bureaus to cardholders each month.

-

Lenders – When you apply for a mortgage or auto loan, ask the lender for your scores from all three bureaus so you can compare.

How to Improve Inconsistent Credit Scores

If you find significant discrepancies in your Equifax, Experian and TransUnion credit scores, here are some tips to align and improve your scores:

-

Dispute errors – If there are mistakes dragging one score down, dispute them with the bureau and creditors.

-

Pay down balances – Reducing credit card balances can quickly boost a low score.

-

Ask for score recalculations – If errors are fixed or balances paid down, ask bureaus for an updated score.

-

Build healthy credit habits – On-time payments and low balances will improve all your scores in the long run.

-

Monitor regularly – Check reports and scores every few months to fix issues before they spread.

The Bottom Line

It’s normal for your Equifax, Experian and TransUnion credit scores to differ somewhat. But by monitoring all three regularly and disputing errors, you can align your scores and put your best foot forward with lenders. Focus on building consistently healthy credit habits, and your scores will reflect it over time.

How Experian Works

Experian breaks its credit reports into sections, which include the following:

- Personal information, including past addresses.

- Employment.

- Accounts, which include credit cards, loans, mortgages.

- Inquiries, which include any creditors checking a report due to a recent application.

Experian provides monthly data for each account, including the minimum payment due, payment amounts, and balances. Its reports indicate how much longer any given account will remain on the credit history and also list the monthly balance history for each account.

More companies use Experian for credit reporting than use Equifax. This alone does not make Experian better, but it does indicate that any particular debt is more likely to appear on an Experian reports.

How Both Credit Bureaus Work

Credit bureaus collect data on individual consumers that is supplied to them by creditors, such as banks, mortgage lenders, and credit card companies. They assemble that data into credit reports, which list credit accounts the individual has opened or closed, as well as their month-by-month payment history within the last seven years.

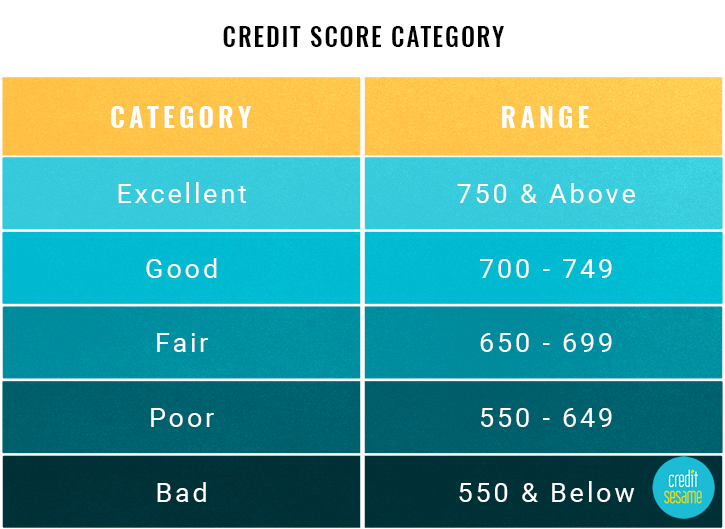

Based on that credit history, credit scoring companies can create a numerical measurement of a persons creditworthiness. Credit scores scores typically range from 300 to 850, depending on the model used to create them. The oldest and most widely used scoring system is the FICO score from the Fair Isaac Corporation. A newer competitor is the VantageScore, jointly developed by Equifax, Experian, and TransUnion, the smallest of the big three credit bureaus.

A credit score can affect whether someone will get approved for a credit product, such as a loan or credit card. Credit scores are also used by lenders to determine the size of a loan theyre willing to make as well as the interest rate to charge the borrower. Credit scores can even come into play when someone applies for a job, an apartment, or an insurance policy.

Experian and Equifax collect some of the same basic information, including:

- Personal data, such as name, birth date, address, and employer.

- Account summaries of loans as reported by creditors.

- Public records, which list any judgments against the person, as well as bankruptcies and IVAs (individual voluntary arrangements).

- Previous credit checks and inquiries from creditors, including a list of all of the credit applications that have been made by the borrower.

Its important to note that not all lenders supply information to both of these credit bureaus. A particular account may appear on one bureaus report but not on the others. So their reports may differ, as can the credit scores that are derived from them.

In addition, lenders often use their own credit scoring models and may arrive at different scores based on the same information.

Why is my Experian score so much higher than Equifax?

FAQ

Why is my Equifax score higher than Experian?

Every credit agency collects own data and determine the credit score. They may not use the same sources. Most of the time, all three agencies give the same score. If there is a big difference, it means that one agency has information that the other two do not.

Is Equifax or Experian more accurate?

Neither Equifax nor Experian is definitively more accurate than the other. Both are major credit bureaus that provide credit information to lenders, but the specific information they hold and the way they calculate credit scores can differ.

Do lenders use Experian or Equifax?

Lenders can use credit reports from any of the three major credit bureaus: Experian, Equifax, and TransUnion.

Do banks use Equifax or Experian?

Credit reporting agencies provide credit reports to lenders, aiding them in assessing loan applications. Among the prominent agencies banks use are Equifax, illion, and Experian. Each agency has its privacy policy detailing how your information is handled.