A credit score is a three-digit number that gives lenders an idea of how likely you are to repay a loan on time. Most scores fall between 300 and 850. The higher your score, the better you look to potential creditors. So what does a credit score of 735 mean for your financial situation?

An Overview of Credit Score Ranges

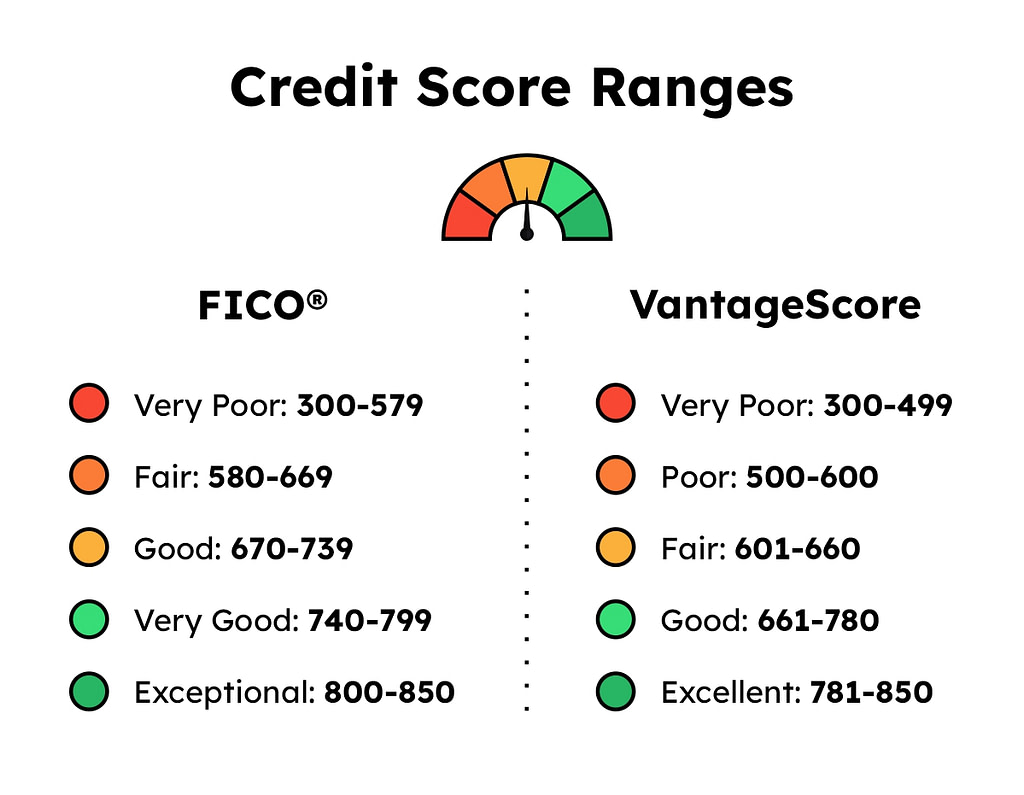

There are a few different credit scoring models, with FICO and VantageScore being the most commonly used. Here is how the score ranges break down according to Experian

- Exceptional: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

As you can see, a score of 735 falls into the “good” credit range. This means lenders will likely approve you for credit, but you may not get the absolute lowest interest rates or best terms. However, a 735 credit score is still above average.

Experian data shows that the average FICO score in the U.S. S. is 714. Since your score is 735, you’re doing better than a lot of people when it comes to your creditworthiness.

What a Score of 735 Means for Credit Card and Loan Approvals

A 735 FICO score is good enough to get most credit cards and loans, but it’s not high enough to get you the lowest interest rates.

Credit Cards

At 735, you should have a decent selection of credit card offers. You can likely get approved for standard rewards cards and cards for good credit from major issuers like Chase Capital One Citi, and others. Prime cards with big sign-up bonuses may still be out of reach unless you have a high income.

The key is to apply only for cards you’re confident you can get approved for. Too many application inquiries can drag down your score temporarily. Also make sure to keep balances low and pay on time every month.

Personal Loans

Personal loan lenders will approve borrowers with credit scores in the good range. However, interest rates may be higher compared to applicants with very good or exceptional scores. Avoid payday loans or high-interest loans that can lead to debt problems. Aim for reputable lenders that offer fair rates based on your credit profile.

Mortgages

If your credit score is 735, you can still get a conventional mortgage, but you won’t have as many options as people with higher scores. For some lenders’ lowest rates, you need a score of at least 740 or 760. Shop around among various lenders to find the best deals. Making your mortgage payments on time can also help your score over time.

Auto Loans

A score of 735 is enough to get approved for a car loan, but you’ll likely wind up with a higher interest rate than borrowers with excellent credit. Rates vary significantly across lenders, so compare offers. Bringing in a qualified co-signer with great credit may help you snag better terms.

How to Improve Your 735 Credit Score

While a 735 credit score gives you access to credit, improving your score could help you qualify for better rates and terms. Here are some tips:

-

Pay bills on time. Payment history is the biggest factor in your scores. Stay on top of due dates for credit cards and loans. Set up autopay or reminders to avoid mistakes.

-

Lower credit utilization. Most of the time, owing more than 10% of your limit can lower your score. Pay down balances and keep usage low.

-

Mix up credit types. Lenders like to see installment loans (mortgages, auto, student) and revolving accounts (credit cards) in your profile.

-

Limit hard inquiries. Only apply for credit you need to avoid too many inquiries. Comparison shopping for a mortgage or auto loan within a short period results in fewer hits to your score.

-

Correct errors. Dispute and remove inaccurate negative items dragging down your credit reports.

-

Become an authorized user. Ask a friend or relative with great credit to add you as a user on a credit card account. Their good history can give your score an immediate boost.

-

Monitor your reports. Keep tabs on your credit by checking your reports regularly so you can catch and correct problems early.

What a 735 Credit Score Means When Applying for Credit

While it’s smart to work on increasing your credit score over time, a 735 already gives you decent access to credit. Here’s a quick rundown of what to expect when applying for different types of credit with a 735 score:

-

Credit cards – Approval highly likely for cards suited to good credit. Prime rewards cards may require an Excellent score of 750+

-

Personal loans – Approval possible from most lenders but interest rates could be higher than with a very good or exceptional score

-

Mortgages – Eligible for conventional loans but may need to shop around for the best rates

-

Auto loans – Qualify for financing but will get lower rates with a score of 760+

-

Apartment rental – Strong approval odds in most cases, but luxury buildings may require a higher score

The higher you can push your credit over time, the better. But in the good credit range, you already have options. Monitor your credit, make payments on time, keep balances low, and take steps to continuously improve your profile. With smart credit management, you can turn that 735 score into something even better.

What Does a 735 Credit Score Mean?

Lenders consider a 735 FICO score to be a “good” credit score. Credit score ranges are usually from 300 to 850, with higher scores indicating better creditworthiness. Here’s a breakdown of credit score ranges:

• Poor: 300-579

• Fair: 580-669

• Good: 670-739

• Very Good: 740-799

• Excellent: 800-850

A FICO credit score of 735 falls within the “Good” range, meaning you have a solid credit history. Lenders often offer favorable terms, such as lower interest rates, to individuals with scores in this range. It’s also bordering on the “Very Good” category, meaning you could have an even better standing credit-wise by building your score by five points.

Quick Tip: Some personal loan lenders can release your funds as quickly as the same day your loan is approved.

How to Get a 735 Credit Score

Borrowers can achieve a “good” credit score of 735 through healthy financial practices:

• Payment history: Timely payment of bills, including credit cards, loans, and other debts, is crucial. Late payments or defaults can damage your score.

• Credit utilization: This is the ratio of your credit card balances to your credit limits. Maintaining no more than a 30% credit utilization rate (closer to 10% is even better) demonstrates responsible credit management. For instance, if you have a credit card with a limit of $10,000, spending $3,000 or less monthly with it can help build your credit score.

• Length of credit history: The longer your credit history, the better. For example, getting a credit card at 20 years old, paying it on time, and keeping the account open can be a positive vs. closing a line of credit you don’t use that often.

• Credit mix: A diverse mix of credit types, including credit cards, loans, and mortgages, can have a positive impact on your credit profile.

• New credit: Opening multiple new credit accounts within a month or two may be risky from a lender’s perspective. Be cautious about applying for too much credit within a short timeframe.

Credit Score Explained

FAQ

How good is a credit score of 735?

Your 735 credit score puts you solidly in the mainstream of American consumer credit profiles, but some additional time and effort can raise your score into the Very Good range (740-799) or even the Exceptional range (800-850).

How to go from 735 to 800 credit score?

We just listed the five factors so let’s go over each one and see how that gets you to 800. Pay on Time. It helps to be a perfectionist, but you don’t have to be to join the 800 Club. Limit Credit Use. Mix and Match Methods of Borrowing. Credit History Matters. Don’t Apply for Credit ….

Can I get a loan with a 735 credit score?

A credit score of 735 is considered excellent and indicates to lenders that you are highly likely to repay your debts responsibly. Because of this, lenders are more likely to give you personal loans with low interest rates and easy terms for paying them back.

Can I get a mortgage with a 735 credit score?

You can generally get a loan with credit scores above the mid-600s. But having scores in the mid-700s or higher increases your chances of securing a competitive interest rate. FHA loans: These mortgages are provided by private lenders but are insured by the Federal Housing Administration.