One of the biggest questions people have when they want to buy a $300,000 house is how much to put down. The down payment is the part of the home’s price that you pay for in full instead of putting it into a mortgage loan. It’s an important factor that affects everything, from your loan options to your monthly payments. What amount of money do you think is a good down payment for a $300,000 house?

The answer depends on your personal finances and goals. But generally a good down payment on a $300K house ranges from 3-20% of the purchase price. Here’s a detailed look at the pros cons, and strategies for different down payment amounts.

Low Down Payments (3-5%)

More and more first-time homebuyers and people who want to buy sooner rather than later choose to put down 3% to 5% of the initial purchase price.

Pros

- Lower barrier to entry. A 3-5% down payment requires less cash upfront. This makes homebuying more accessible.

- Smaller impact on savings. You can keep more of your cash reserves intact rather than depleting them on the down payment.

Cons:

- Higher monthly costs. With less equity in the home, your mortgage payment and mortgage insurance premiums will be higher.

- Potentially higher rates. Some lenders charge slightly higher interest rates on low-down mortgages to offset risk.

Strategies:

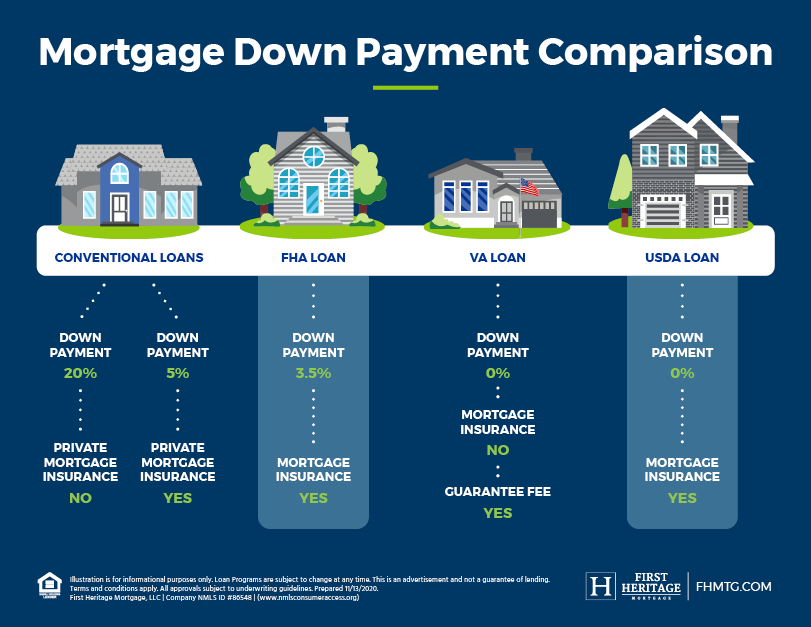

- Conventional 97 loan – Allows as low as 3% down with good credit

- FHA loan – Requires just 3.5% down and is more lenient on credit scores

- Down payment assistance programs – Can provide grants, loans, or other help for the down payment

A 3% to 5% down payment of $9,000 to $15,000 on a $300,000 home can be a good choice if you want to buy faster or save more cash. But be prepared for potentially higher monthly costs.

Moderate Down Payments (10-15%)

Putting 10-15% down has long been seen as the “sweet spot” that balances affordability with monthly savings.

Pros:

- More equity and potential savings. You’ll build equity faster and can request PMI removal sooner.

- Potentially lower rates. 10%+ down payments may qualify for better rates with some lenders.

- Lower monthly costs. More down means less borrowed, so mortgage payments are lower.

Cons:

- Requires significant cash. $30,000-$45,000 down is still a lot for many first-time buyers.

- Less cash remaining. Your reserves will take a larger hit, even if monthly costs drop.

Strategies:

- Conventional loan – 10% down avoids PMI with many lenders

- FHA loan – Allows down payments as low as 10%

- Save diligently – Set specific monthly savings goals to reach 10-15% down

Putting down 10% to 15% strikes a balance between being able to afford things today and saving money in the long run. For many buyers, it’s an optimal amount.

High Down Payments (20% or more)

A down payment of 20% or more has long been the gold standard advice for homebuyers.

Pros:

- No PMI required. Avoid mortgage insurance costs that can add hundreds per month.

- Best rates. The lowest rates are available to buyers with 20%+ down.

- Lower payment. With more equity upfront, your monthly mortgage is significantly reduced.

Cons:

- Requires substantial cash. $60,000+ down will be out of reach for many first-time buyers.

- Major impact on reserves. Tying up this much in your down payment can limit your emergency funds.

Strategies:

- Conventional loan – Requires 20% down to avoid PMI

- Save aggressively – Make major cutbacks and lifestyle changes to ramp up savings

- Delay buying – Take extra time to amass a larger down payment

Over 20% down is ideal in many ways, but may require unrealistic sacrifices for some buyers. Evaluate your own situation carefully.

The Optimal Down Payment Amount

When determining the right down payment for a $300K home, consider these key factors:

-

Affordability – How much can you reasonably afford to put down now without draining all your savings?

-

Monthly costs – Will a larger down payment significantly reduce your monthly mortgage payments?

-

Loan options – Does a certain down payment amount open up better loan programs and interest rates?

-

Timeline – How soon do you need to buy? Can you delay to save more?

-

Goals – Are you focused on buying quickly, minimizing costs, or building equity fastest?

Carefully weighing all these elements will help you land on the ideal down payment for your $300K home purchase. A good rule of thumb is to put down as much as you comfortably can while staying within your budget.

While there’s no single right answer, following prudent financial guidelines will set you up for success. With smart planning, even first-time homebuyers can make a down payment that fits their needs and gets them into the home of their dreams.

Loan Amount, Down Payment, and Mortgage Payment Tables

The tables below outline four different down payment options and loan amounts, as well as the related mortgage payments for all those loan amounts – with four different interest rate scenarios. The purpose of this is to give you an understanding of how much interest rate movement will impact your mortgage payment.

Note that these calculations assume that the mortgage is amortized over 30 years, and the payments do not include property taxes, homeowners insurance, mortgage insurance (for FHA), or private mortgage insurance (PMI). PMI, once again, is usually required for mortgages associated with down payments under 20%.

Down Payment Options and Corresponding Loan Amounts

- 3% Down Payment: $9,000 down; $291,000 loan amount

- 5% Down Payment: $15,000 down; $285,000 loan amount

- 10% Down Payment: $30,000 down; $270,000 loan amount

- 20% Down Payment: $60,000 down; $240,000 loan amount

Can You Actually Afford a $300,000 Home?

FAQ

How much should I put down on a $300K house?

… buy a $300,000 house with $60,000 down with any mortgage loan, but most buyers opt for a Putting $60,000 down on a $300,000 house—that’s a 20% down payment …Apr 25, 2025.

What is the minimum income to buy a 300K house?

There is no one-size-fits-all answer, but a salary of $75,000 to $95,000 a year is a good place to start for buying a $300,000 home. But keep in mind that this is a rough estimate.

Can I afford a 300K house on a $70K salary?

Can I afford a $300K house on a $70K salary? If you have minimal debts then a $70,000 salary might be enough to afford a $300,000 house. The size of your down payment and your mortgage interest rate will be important variables. Try to keep your monthly house payments below a third of your monthly gross income.

How much do you need to put down to build a 300K house?

Conventional loans typically require 3-20% down for a 300k house. Government-backed loans like FHA, VA, and USDA have different down payment requirements. Your down payment affects your monthly payments, interest rates, and additional costs like PMI.